#5 - NOVEMBER 2025

Towards the end of globalisation ?

It looked like a decided trend. But the 2008 crisis dealt it a hard blow. Since then, globalisation seems to have stalled. Welcome to the era of slowbalisation.

Laurent Ferrara

Professor of International Economics

SKEMA Business School

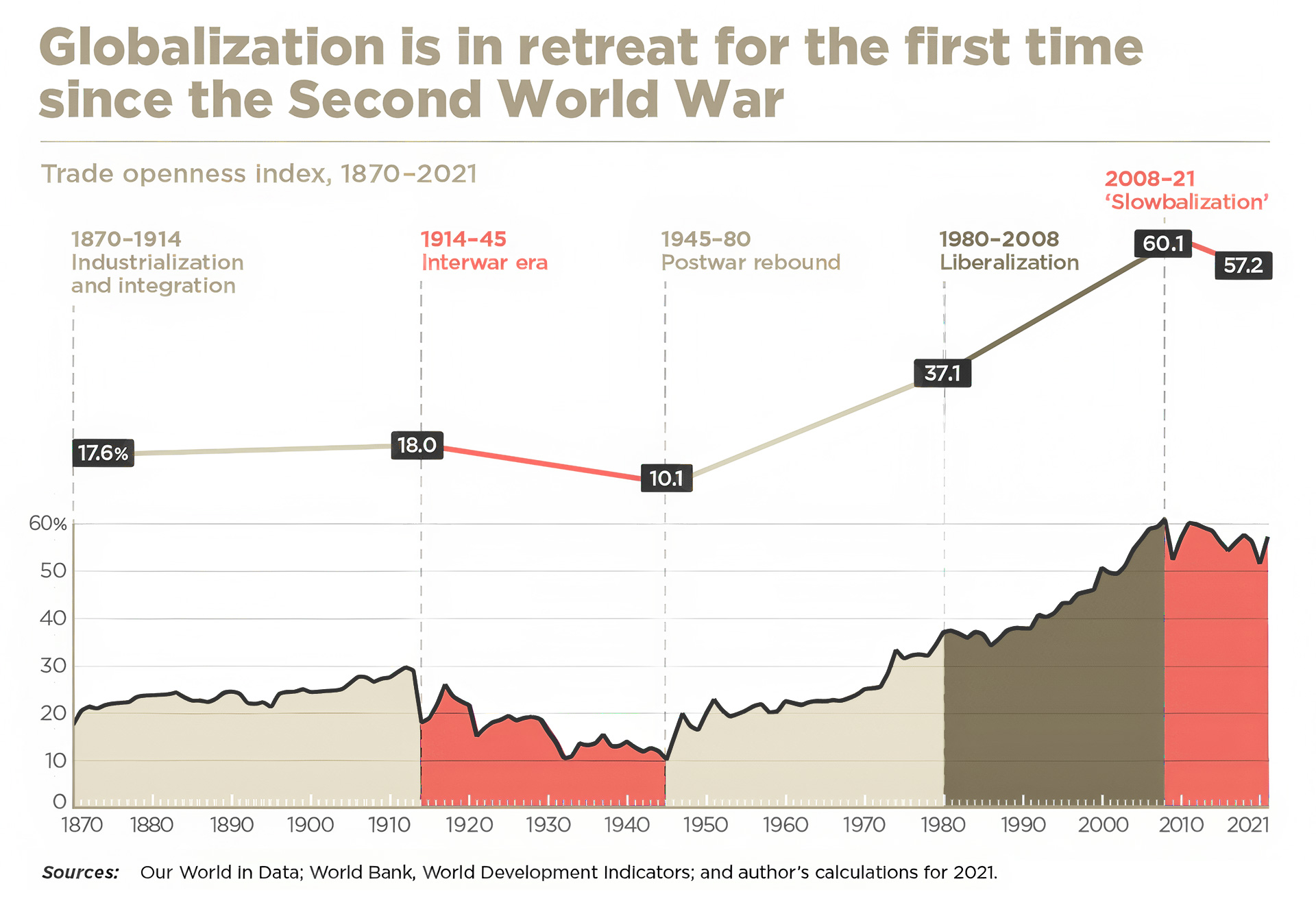

The globalisation of trade between countries around the world is generally measured by the trade openness index, calculated as the sum of global exports and imports of goods divided by the global GDP. The graph showing the variations in this index since 1870 shows that the global economy has seen five major phases (see graph).

A five-step waltz

Firstly, a 20% to 30% increase between 1870 and 1914, due to the industrial revolution, and the growing trade in finished consumer goods and raw materials between advanced and developing countries respectively. The First World War brought this initial phase of globalisation to an abrupt halt.

The third period began at the end of the Second World War, triggered by post-war reconstruction and the Washington Consensus, which encouraged countries to liberalise and open up to the rest of the world. However, this globalisation remained incomplete, given the emergence of two major blocs: the Western countries operating on a market economy versus the communist countries of the East. The non-aligned countries of Africa, Asia and Latin America formed a third bloc, thereby limiting global trade.

Globalisation accelerated rapidly in the early 1990s after the collapse of the Communist bloc and the incorporation of emerging countries into global value chains. In particular, China’s integration into the World Trade Organisation (WTO) in 2001, combined with a massive drop in transport costs, led to a huge surge in goods trading, particularly intermediate goods used in the manufacture of other items.

In 2008, the trade openness index stood at 60%. 2008 was a key date because it marked the biggest global economic crisis since the Great Depression of 1929, though industrialised countries were more severely affected than emerging countries.

Since then, globalisation has never regained its growth momentum, and the trade openness index has stabilised at around 58%. The World Bank’s latest official data for 2024 shows an index of 57%.

2008: the end of a world?

Why has trade been stagnating since 2008? Several factors explain this. Firstly, the global economy has seen a series of economic recessions with a collapse in overall demand (the 2007 financial crisis, the 2012-13 eurozone debt crisis, the Covid pandemic, the war in Ukraine and global inflation since 2022), which has significantly reduced cross-border trade, at least in a greater proportion than global GDP.

Secondly, the current trend is moving towards a return to protectionist policies designed to protect domestic production at the expense of imports. The most symbolic measure is obviously the increase in customs tariffs rolled out in the US by the Trump administration from April 2025 onwards, which has increased the cost of American imports. Other non-tariff-related measures may be implemented to limit cross-border trade, like subsidies for local production, bank loans at highly favourable rates, or simply changes in standards.

This new international trade landscape has its roots in geopolitical tensions between major countries, which are now tending to organise themselves into blocs and enter into bilateral trade agreements rather than bend to the rules of a multinational body like the WTO. This has led to what is known as the “fragmentation” of international trade between countries or blocs that share common values. The US is gradually withdrawing from numerous international organisations and isolating itself from the rest of the world. Meanwhile China is aiming to become the leader of a bloc of emerging countries based on the BRICS states (Brazil, Russia, India, China and South Africa). For several years now, these countries have been meeting with other emerging and developing countries in an attempt to strengthen their economic and financial ties, even though their chief common factor seems to be the desire to oppose Western countries. Between these two major blocs, there is still room for Europe to exist, but this will require significant reforms and massive investment in climate transition and new technologies, as highlighted in Mario Draghi’s 2024 report.

Given the extent of integration of global value chains, it seems unlikely that we will see a sharp decline in the trade openness index in the short term. Trade is more likely to stabilise in line with a marked fragmentation of trade flows between large geographical blocs. In the longer term, geopolitical relations will certainly shape the geography of trade flows in goods and services alike.